The travel and tourism industry will experience long-lasting domino aftermath shocks across the whole tourism value chain, with recovery timelines between 5-10 years for some categories, as a result of the Coronavirus (COVID-19) crisis. The impact of the pandemic on airlines has been huge, from the grounding of entire fleets to increasing debts and worsening liquidity, leading to poor aircraft occupancy and floods of cancellations and refund requests.

According to the International Air Transport Association (IATA), the airline sector has taken a major hit, with projections for revenue loss of USD$84.3 billion in 2020 and a decline of passenger travel of over 50% compared to 2019.

Halted for more than four months, the industry is veering close to complete collapse as a result of suspended operations, low demand and an extremely uncertain business landscape following mandatory quarantine imposed by individual governments where international travel is permitted, or “stop-go-stop” travel restrictions which lead to further cancellations and chaos for both passengers and carriers. As a result, many carriers are facing not only insolvency problems but potentially a completely reconstituted industry.

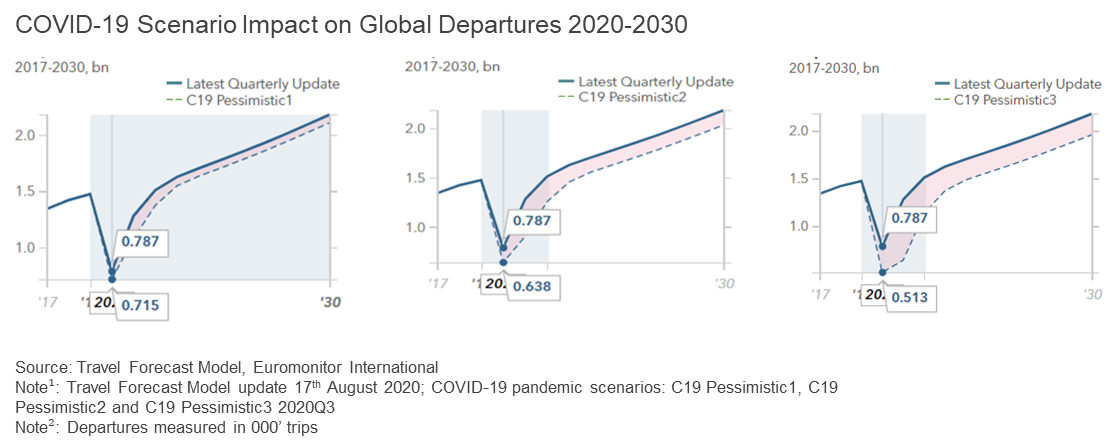

Global departures drop, hitting aviation hard

The future progression of airlines is closely linked to the recovery timelines for global departures in a post-lockdown environment. The assessment of this data is therefore based on the latest update of the Euromonitor International Travel Forecast Model, with potential for these trends to progress even further downwards if the situation worsens globally as demonstrated by our three Pessimistic COVID-19 scenarios.

With a volatile job market and skyrocketing unemployment, disposable income is likely to see a major negative impact, translating into slower rates of both leisure and business travel, as consumers trade down, focus on savings and avoid expenditure on non-essential products and services. This, of course, will not lead to a complete halt in consumer demand and travel services but rather change the way people travel, their behaviour and preferences.

Domestic market – the panacea for the transportation recovery

The domestic market is seen by many players in transportation as the panacea for the recovery of their operations, in addition to the financial relief they receive from their respective governments. Domestic travel worldwide is projected to reach 18 billion trips by 2025 compared to 12.9 billion in 2019, according to Euromonitor International. Importantly though, not all companies have a domestic market share; this is especially relevant for airline operators, preventing them from rebuilding capacity.

Source: Euromonitor International. Note: Domestic travel measured in terms of number of trips.

• With large domestic airline markets, Asia Pacific (the region first affected by the pandemic) is already seeing an anaemic but encouraging rebound, especially in China, South Korea and Vietnam. Domestic markets are projected to rebound quicker as internal travel restrictions in many countries are lifted.

• Carriers such as Korean Air, Vietnam Airlines and AirAsia have already started the operation of domestic flights, albeit at much lower capacity compared to the same period in 2019. This, however, represents green shoots of slow recovery for the industry.

Flight protocols changing

As travel restrictions ease and social distancing measures become more relaxed, many operators have started to rethink their safety practices onboard aircraft as well as other changes in response to the pandemic:

• Stringent sanitising including electrostatic spraying (eg United Airlines), new boarding protocols and compulsory protective clothing such as masks and gloves are being made a requirement for travellers.

• Immunity passports featuring COVID-19 test results, as well as infrared body temperature checks (eg Korean Air) are some of the additional actions expected to be introduced by operators. Improved filtration systems and disinfectant fogging are further protection measures being discussed by the trade. Middle seat booking restrictions are also widely adopted a policy with airlines such as Qantas, American, Alaska Airlines, while others are waiving their change and cancelation fees in a bid to stimulate bookings.

• With projections for a rebound for the airline sector of at least five years as a result of low demand and ongoing travel restrictions, many carriers are starting to consider huge capacity reductions, as well as a shift towards their major hubs, prompting a review of those routes which are not profitable. With the aim of achieving strong cost savings, carriers are expected to include frequency reductions and shift towards domestic air on the back of visiting friends and family traffic, which is expected to recover fairly quick as part of leisure travel. To stimulate demand, many players are expected to lower fares in order to encourage more travellers on board, but also due to relatively high overcapacity in the market and aggressive competition on key routes.

Crisis takes its toll on airports too

• Airports are an integral part of the air transportation sector and as with airlines, airports have been hit particularly hard by the pandemic and lockdown. According to Airports Council International’s (ACI), more than 4.6 billion passengers will be lost in 2020, with Europe and Asia Pacific seeing the biggest dives, whilst airport revenues will decline over USD97 billion by the year-end of 2020.

• With commercial activities paralysed, anaemic duty-free retail and minimal income from airport charges, many operators are fighting for survival. Adhering to new health protocols and social distancing measures whilst trying to ensure a seamless customer experience at the airport will be a major challenge. Contactless technologies, AI, biometrics, thermal sensing, electronic bag tagging, as well as real-time management of passenger and baggage flows and increased sanitation will be essential for operations in the post-COVID-19 environment. This, in turn, will require additional high-cost investments to enable airport players to become fully digitalised entities that can have full control of the whole passenger journey at the airport.

Learn more in our white paper: Travel 2040: Sustainability and Digital Transformation as Recovery Drivers.