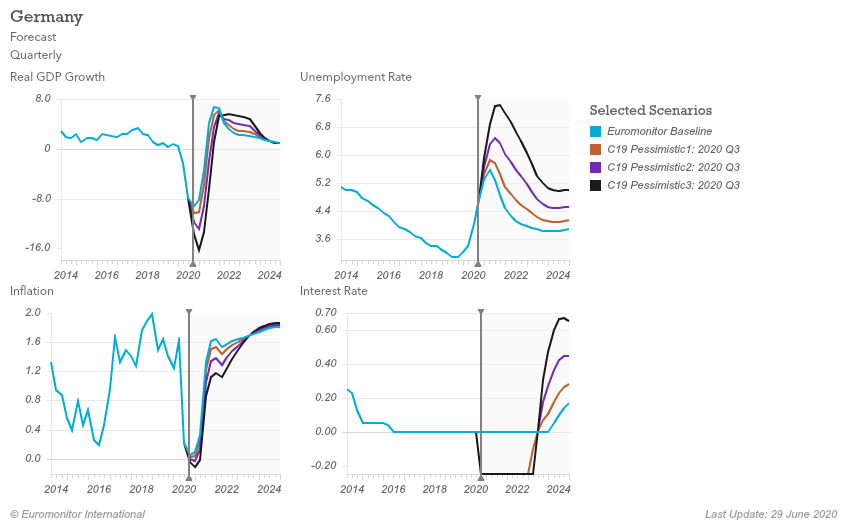

After a decade of consecutive growth, the German economy officially entered recession in Q1 2020 as the Coronavirus (COVID-19) pandemic hit, with the biggest slump expected in Q2 before a gradual path towards recovery from Q3 onwards. Germany has not had as strict a lockdown as many of its European neighbours. Schools, non-essential shops and borders all closed in mid-late March, and there was a ban on contact (Kontaktverbot), which meant people could not gather in groups but could meet up with one other person from a different household. However, there were no restrictions on going outside the home in most places. From late April, non-essential shops and foodservice outlets, as well as schools, were gradually allowed to reopen, whilst observing social distancing rules.

Although the government has quickly implemented a large rescue package and gained initial success through relatively loose movement restrictions, culminating in retail stores reopening in May, the country’s large export-oriented manufacturing sector is suffering due to weakening external demand. The temporary closure of non-essential businesses, coupled with a dip in manufacturing and consumption, are also hurting employment, with the unemployment rate rising significantly in 2020, contrasting with a record-low level in 2019. Consumer sentiment is falling, and per capita disposable income is expected to decline by 6.4% in real terms in 2020. Faced with these challenges, already cautious German consumers are becoming even more prudent and selective with their spending.

Germany’s Quarterly Macroeconomic Forecasts with COVID-19 Scenarios: 2014-2024

Source: Euromonitor International’s Macro Model

Yet, the fast-changing environment has also fostered agile innovations from businesses in Germany, as they adapt to disruptions to supply chains and shifts in consumer needs and habits. Some big-name companies have diverted their production and developed new business models, while companies have also shifted their strategies from profit to purpose in these unprecedented times, particularly given the increased scrutiny from German consumers, who have been critical of companies not deemed to be practising solidarity.

Consumer payments: COVID-19 crisis accelerates card and mobile payments

Consumer spending in Germany is still largely conservative, with a lot of consumers opting for cash payments for their daily purchases and electronic direct transactions for scheduled payments. There is still a general reluctance towards making payments with cards – seen as more challenging to keep track of spending – let alone with a mobile device. However, the COVID-19 crisis – as the global pandemic is locally referred to in Germany – has served as the catalyst that will accelerate the shift away from cash payments in 2020.

Overall, weaker consumer confidence and tighter budgeting is projected to result in an overall decline in consumer payment transaction value in 2020. There has been a jump in card payment transactions, largely due to hygiene considerations. Based on the World Health Organisation’s recommendation to avoid cash transactions in order to mitigate the spread of COVID-19, more merchants in Germany have encouraged customers to use payment cards. While the ubiquitous girocard debit card already posting record transaction growth in 2019 before the outbreak, the pandemic has led to an additional jump in card payments, especially contactless transactions, which an increasing number of consumers view as the safest option. This new payment behaviour is likely here to stay, particularly with a jump in the number of outlets within previously cash-dominant domains, such as bakeries and weekly markets, introducing card payments.

Strong brakes on out-of-home spend in German retailing landscape

Within the German retailing landscape, the COVID-19 crisis has had a disruptive impact. Starting mid-March and continuing to late April, the government imposed the closure of physical stores deemed as non-essential, ie all outlets except for grocery retailers, pharmacies and drugstores, resulting in massive sales losses. Yet, even with all stores reopening from late April onwards, footfall has remained considerably lower compared to before the pandemic.

Amidst the woes of most store-based retailers, e-commerce saw sales surge in April, following a significant contraction in March, thereby posting positive cumulative growth for March and April compared to 2019. This was driven especially by food and drinks e-commerce as well as online sales from pharmacies and drugstores. E-commerce sales in Germany overall are still performing below their potential, especially for grocery products, and while e-commerce growth continued to be favourable up to 2019, the COVID-19 crisis has fuelled the online shift. On the whole, retailing value sales in Germany are expected to shrink for the whole of 2020, despite the growth seen across grocery, pharmacies, drugstores and e-commerce channels, because the increase in sales from these channels will not be sufficient enough to compensate for the much-reduced spending in non-essential stores.

Out-of-home purchases simply went into freefall due to the COVID-19 pandemic – first with the halt of inbound travellers from February particularly from outside Europe, even prior to border closures in mid-late March, followed by the closure of consumer foodservice outlets and travel restrictions from mid-March onwards. Through the “soft lockdown” period from mid-March to May, most away-from-home trips made by consumers were limited to the few retail places that remained open for the purchase of essential goods, while non-essential services out-of-home were severely restricted by both outlet closures and by consumers’ new spending priorities. Government-enforced lockdown between March and May effectively shut down all aspects of tourism, for example, while foodservice places were restricted to takeaway and delivery orders. The value of non-essential services away-from-home is unlikely to reach pre-crisis levels in the short term given the drawn-out effects of economic recession on discretionary spending.

Forecast Baseline Value Sales Growth in the Best- and Worst-Performing Consumer Industries in Germany: 2020

Out-of-home experiences: Consumer foodservice home delivery and domestic travel benefit

The COVID-19 crisis has hit out-of-home expenditure in Germany hard in 2020, ranging from spending on travel to eating and drinking. Despite the lack of inbound travellers and internal movement restrictions affecting Q2 2020 hardest, value sales for the entire year are projected to decline at a double-digit rate – estimated to be between 15-20% – and the recovery period is likely to be prolonged into 2021 onwards.

Within consumer foodservice, over 75% of spending in 2019 catered to dine-in traffic. By April 2020, only takeaway, drive-through and home delivery services could be made available to consumers, severely hurting those restaurants that lacked access to or expertise in delivery as a service. Restaurants were open again by late May but physical distancing restrictions will have a strong impact on operational capacity and in-store atmosphere, which is likely to dampen the enthusiasm consumers have for dining in. As such, 2020 sales as a whole are projected to shrink by over 10%.

Moving forward, restaurant delivery will likely see the most rapid transformation in Germany. Delivery sales that were relatively low compared to most other Western European markets will likely accelerate, as foodservice operators look for ways to offset severe declines in dine-in traffic. Even as dine-in traffic slowly returns to normal over the long term, delivery adoption is here to stay as restaurant expertise and consumer adoption solidify.

Foodservice Orders by Occasion in Germany: 2019 Value Sales Breakdown

Source: Euromonitor International Consumer Foodservice

Within the travel industry, inbound arrivals to Germany are projected to fall by 61% compared to 2019 by year-end 2020, according to the Travel Forecast Model C-19 Pessimistic1 scenario, with expenditure from inbound travellers projected to shrink by over 20% during the year as a whole. Domestic travel in contrast, following several months of restrictions, is poised to normalise more quickly, surging to above-average levels in the second half of 2020 as consumers have both the pent-up urge to travel, but not too far from home, as well as annual leave days that were unused in the first half of the year. The warm summer months will see demand in the coastal resort destinations of Mecklenburg-Vorpommern and Schleswig-Holstein, and camping, hiking and other nature-based trips in the country’s interior. As such, the rate of decline in trips is likely to be significantly less than that of outbound travel, and domestic travel expenditure is set to only drop at a single-digit rate during 2020 overall.

Cross-border travel is likely to normalise in Germany’s neighbouring countries by year-end 2020, with broader travel across the Schengen Area picking up in early 2021. German holidaymakers will once again return to places along the Mediterranean and Aegean seas where tour operators like TUI have the most to offer in terms of packaged holiday opportunities. Meanwhile, long-haul trips are likely to be seen as posing the biggest risk. Outbound travel is likely to drop the most, with a 35-40% decline in the number of trips in 2020 and only returning to pre-COVID-19 levels in 2022.

Inbound Arrivals Growth to Germany: 2020

Source: Euromonitor International’s Macro Model – Travel Flows. Note: Data from 2020 are forecasts.

Food and drinks: Strong shift from consumer foodservice to retail

Although overall packaged food volume sales in 2020 are forecast to decline by 1%, matching the growth trajectory seen in previous years, this hides remarkably mixed fortunes between the retail and foodservice channels. The former is predicted to see a 6% rise in volume terms, while foodservice sales are set to fall by a whopping 23%.

Some categories which relied on on-the-go consumption and performed strongly before the COVID-19 crisis are expected to be strongly hit. Within ready meals, prepared salads, targeting out-of-home consumption, typically lunch in the office, are likely to see a 4% retail volume decline in 2020, while products to keep in the freezer such as frozen ready meals and frozen pizza are forecast to grow by 8%. Sports drinks are similarly expected to fall out of favour with more sedentary consumers, with a stagnation in volume sales, while tea is predicted to see an unexpected recovery, with a 1% rise.

As consumers eat more frequently at home, they will seek to replicate recipes from foodservice outlets with convenient products. This should strongly boost instant noodles and pasta sauces, whose volume sales growth is forecast to reach double digits in 2020. Smaller pack sizes are being undermined by the lack of on-the-go consumption, notably with fewer business trips, while larger pack sizes and multipacks, particularly favoured by online grocery shoppers and useful for stockpiling, could make gains.

Beyond 2020, the growth pattern in packaged food and non-alcoholic drinks is likely to follow a V-shaped recovery, whereby the erratic growth curves will stabilise from 2021, with many categories seeing consumption return to previous or almost previous levels. However, new habits formed during the pandemic crisis will shape longer term-trends, in particular leading to an acceleration of the shift to online grocery shopping. Food and drinks manufacturers are expected to focus on more basic products and those with local provenance, which reassure consumers, and on those allowing them to have affordable treats at home.

Alcoholic drinks and tobacco: Stimulants under pressure

One of the side effects of more German consumers spending more time at home is not only cabin fever (Lagerkoller), but also increasing stress levels brought about by unemployment problems, homeschooling difficulties and other pressures. In Germany, some try to cope with stress by increasing their intake of stimulants such as alcohol, nicotine or even CBD. The contact ban (Kontaktverbot) of more than two people from different households from 22 March up to early June in an attempt to reduce the spread of COVID-19 resulted in the loss of the social aspect of going out and drinking with friends as well as smoking together (particularly important for waterpipe tobacco in Germany). For alcoholic drinks, this is reflected in an expected decline of 30% in on-trade volume sales in 2020. Despite alcohol being seen by some consumers as a way to help them deal with stress, the expected off-trade volume sales growth of 2% in 2020 cannot capture all sales lost in the on-trade environment.

In terms of cross-border sales, many people were not able to legally buy cheaper alcoholic drinks or cigarettes in neighbouring countries. Although border closures within the Schengen Area only took place for a few months (in most cases from mid/end March to mid-June), it has led to decreasing cross-border sales as well as consumers shifting to cheaper categories (eg fine-cut tobacco) within German borders. The lack of cross-border sales are expected to boost sales in Germany and are therefore a key factor contributing to volume growth of cigarettes expected to only stagnate in 2020 in Germany, rather than to decline as previously expected. However, in the long term, illicit trade is expected to play a more significant role as cigarettes are becoming more expensive. This is due to growing attention being paid to tobacco and its impact on respiratory health and the tax increase that is likely to happen.

Relatively swift recovery ahead for Germany, despite “the new normal” expected after the COVID-19 crisis

It is important to highlight that the impact of the COVID-19 crisis on industries in Germany has been less severe than in various other major European markets, due to a strong handling of the crisis, even if it was the trigger to a long-avoided recession. Nonetheless, German consumers are still likely to emerge into a new normal in the post-pandemic world. While a sizeable proportion of German consumers will suffer unemployment and significant loss in income and spending power in 2020, a likewise sizeable proportion of the population has accrued more savings due to reduced spending during the year. Of the trends accelerated in 2020 due to the pandemic, the stronger acceptance and usage of card payments and an uptick in mobile payment is definitely here to stay. The growing popularity of consumer foodservice home delivery is also unlikely to reverse back in the long term, nor is the trend towards food and drink e-commerce. In contrast, the trend for domestic travel and home cooking may wane in the midterm.

Going forward, German consumers are likely to remain cautious in their spending habits: they will likely seek products that provide the reassurance and offer back-to-basics features and value for money over those that offer the most advanced features or design or luxury brands. The “buy local” trend is expected to become more prevalent, as local sourcing is seen as more sustainable and socially responsible by many German consumers, which could encourage them to accelerate changes in their supply chain. In early June, the German government announced a major fiscal stimulus package, including a temporary cut in VAT, reducing the standard rate from 19% to 16% for the second half of 2020 in order to encourage consumer spending for the rest of the year.

Authors: Raphael Moreau, Maxim Hofer, Stephen Dutton, Lan Ha, Linda Lichtmess